GDX weekly

GDX monthly

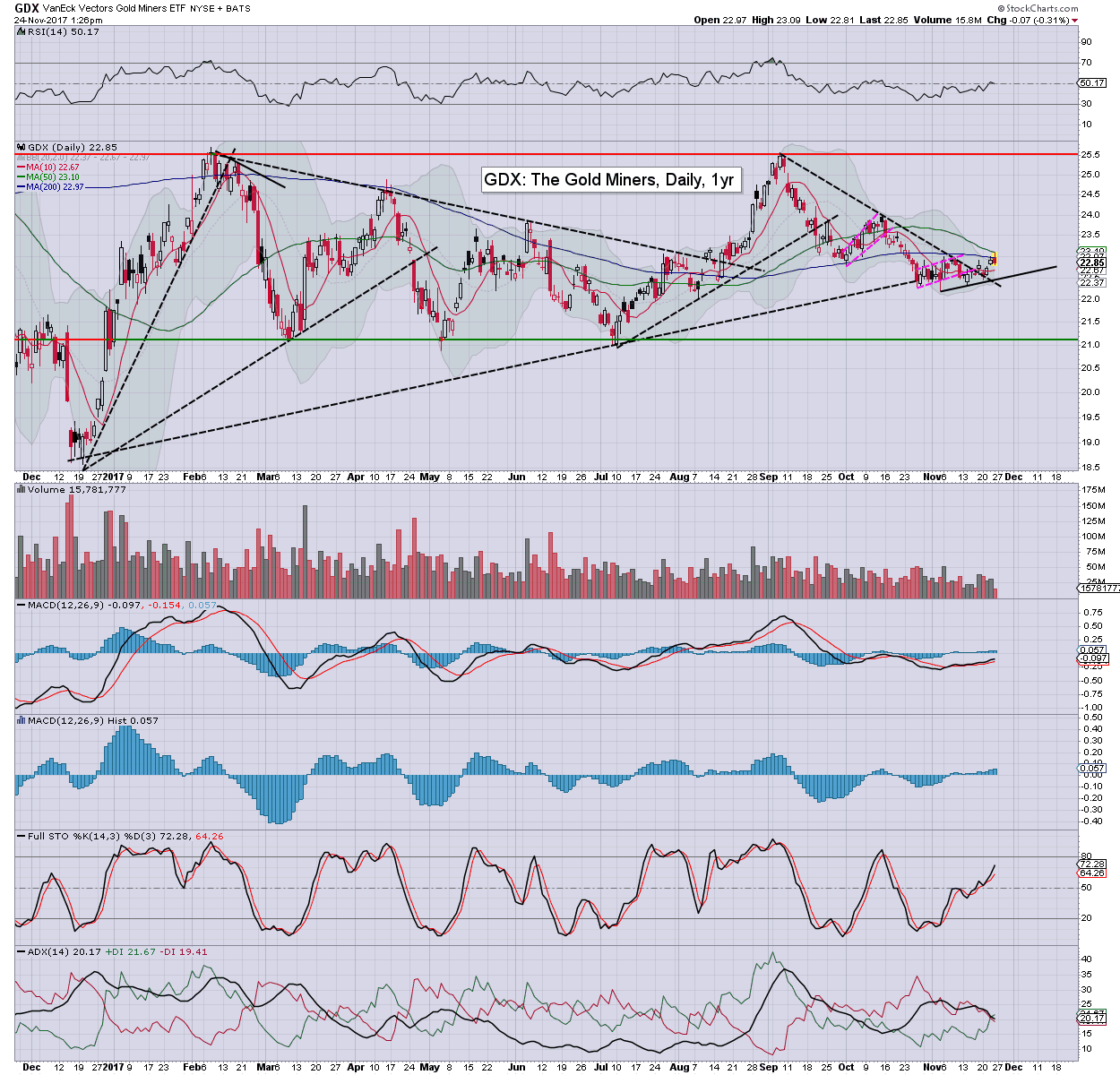

Summary

With the precious metals rising into year end, the miners followed, with a third consecutive net weekly gain. The settling December candle is rather bullish in style, and does offer a push into the $25s within 1-3mths.There was very notable option activity today in GDX, with >59000 of the Feb'16th $25s trading.

| |

| Pete Najarian of investitute.com highlighting unusual activity |

Copper and oil are both indirectly suggestive that gold/silver will eventually battle upward in 2018. If correct, the miners will no doubt follow to some extent.

For bullish clarity, the mining bulls should be seeking Gold >$1400, Silver >$22s, with Copper >$3.00. The latter was achieved in August.

The more cautious will leave GDX alone until the Feb high of $25.71 is taken out. Any price action >$26.00 would then offer a fast run to challenge the summer 2016 high of $31.70.

--

For the record, my favourite gold miner remains...

Barrick Gold (ABX), monthly

Barrick ended the year on a very bullish note, with a Dec' gain of 5.0% to $14.47. Its notable that the Dec' candle is of the bullish engulfing type, and does lean to at least short term upside to the 15/16s. The cautious will wait for a break above trend, which in January will be considerably higher, around $17.30.

It could be argued price structure since summer 2016 to late 2017 is one giant bull flag. Will need to see >17.30 to provisionally confirm that, and >$23.24 to fully confirm it. If the latter was seen, natural target would be the 37/40 zone.