The Gold miners ended the week on a positive note, with the ETF of GDX settling the day +1.1% at $22.81. This was still not enough to manage a net weekly gain, with GDX -0.5%. For the month, GDX settled moderately lower by -0.2%.

GDX, monthly

GDX, weekly

Summary

Suffice to add... March was a mixed month for the precious metals and the related mining stocks.

The mid term trend that links the Jan'2016 and Dec'2016 lows is comfortably intact. Underlying MACD (blue bar histogram) on the monthly cycle continued to tick lower in March, but is levelling out around the zero threshold.

Outlook is for broad upside across the year. First big target is the summer 2016 high of $31.70. Any price action should confirm that $50 will be seen, whether late 2017.. or a far more viable 2018.

Things would only turn bearish with a break under $20.50 in April.

Many were rattled by WTIC oil recently cooling to the low $47s. Certainly, the weakness in oil pressured energy stocks lower, but the downward trend from Dec'2016 looks likely to have concluded. The sector ETF of XLE settled the day u/c at $70.14. Things turn bullish with a break into the $71s.

XLE, weekly

Summary

A rare highlight of the sector ETF of XLE, which I'd argue is a very valid way to trade the energy sector.

XLE peaked in Dec'2016 at $77.57. The weekly candle was itself a black-fail, which are pretty rare for the bigger weekly cycles.. and are almost never seen on the giant monthly cycles.

From the Dec' high, XLE has very consistently declined, and even broke a new low of $67.86 a few days ago.

With WTIC oil back to around the $50 threshold, XLE is battling to settle the week with a very powerful bullish engulfing candle. This is the most bullish candle since at least late Oct'2016.

--

Things turn bullish with a break into the $71s. Once achieved, first target will be the 77/79 zone, and that is a clear 10% higher. Time frame would be within 2-3 months.

--

A subscriber kindly highlighted this to me today...

I'm somewhat familiar with Kimble, and I largely agree with much of the article.

--

Implications for the broader market

Many (myself included) have been seeking a basic 5% retrace within the main equity market. Yet, that is simply not going to be possible if the energy sector is about to push significantly higher. If you believe XLE will climb around 10% within a few months, its difficult to see how the main market will not continue to battle upward.

Whilst the main equity market saw a day of minor chop, there was notable significant strength in the energy sector. Chesapeake Energy (CHK) settled higher by a very powerful 7.8% at $5.81. With today's gain, CHK is now set for a net monthly gain. First big upside target is the $8.00/8.25 zone.

CHK, daily

CHK, monthly

Summary

Today's oil inventories helped give energy stocks an extra kick upward. Even though Chesapeake is Nat' gas focused, it is unquestionably greatly swayed by price action in WTIC oil.

Cyclically - short term, we tested the 50dma today... the 200dma is just a touch high. Things turn very bullish with some price action above declining trend/resistance, which will be around the $6.00 threshold in mid April.

Mid term, CHK looks headed (eventually) for core resistance at the $12 threshold. Its notable even a move to that level would still be a massive way below the levels from summer 2014.

Whilst the main market managed moderate gains, there was more significant strength in Century Aluminium (CENX), which settled +1.9% at $12.41. Near/mid term outlook is bullish, with first soft target of the 50dma around the $14.00 threshold. A break above the Feb' high of $16.53 appears due.

CENX, daily

CENX, monthly

Summary

Like many industrial/material stocks yesterday, CENX saw a rather powerful bullish engulfing candle. This was where the Friday low was taken out, but the stock swung far higher.. closing well above last Friday's high.

Price action since Sept'2016 has been exceptionally bullish. We've now seen 3 higher lows, and 3 higher highs.

Seen on the giant monthly cycle, we can see grander resistance at the $20 and $30 thresholds. Even if CENX were to reach $30/40, that would still be less than half of its commodity bubble high of $80.52.

--

I am very bullish for CENX, along with AA, X, and a fair few other names. All could be termed 'Trump trades', on the outlook of a growing US economy... with some element of commodity inflation.

Whilst the main market battled upward from opening lows, there was particular resilience in SNAP, which settled +4.8% at $23.83. Near term outlook is bullish, as mainstream consensus is for further upside, which would clearly be helped if the sp' can push upward to 2425/50 by early May.

SNAP, daily

Summary

So, the fifth net daily gain of the past six trading days. SNAP has climbed from a cycle low of $18.90, to today's intra high of $24.40. Clearly, these are still very early days for the stock, and the above daily chart only has 18 candles on it.

Its ironic that just a few weeks ago, the mainstream were regularly chatting 'SNAP to $10'. That still seems possible, but not before new highs, probably in the low $30s.

--

Meanwhile... on clown finance TV...

You can see a fair few institutions are currently touting SNAP to $24, with RBC seeking $31. Indeed, the low $30s do seem viable within a month or two, not least if sp'2425/50 by early May.

--

To be clear, I have ZERO interest in meddling in such a stock that is surrounded by such hysteria. Hell, I'd even prefer TWTR over snap, not that I'd meddle in that mess either.

SNAP is certainly an interesting one to follow... if only for 'entertainment purposes'.

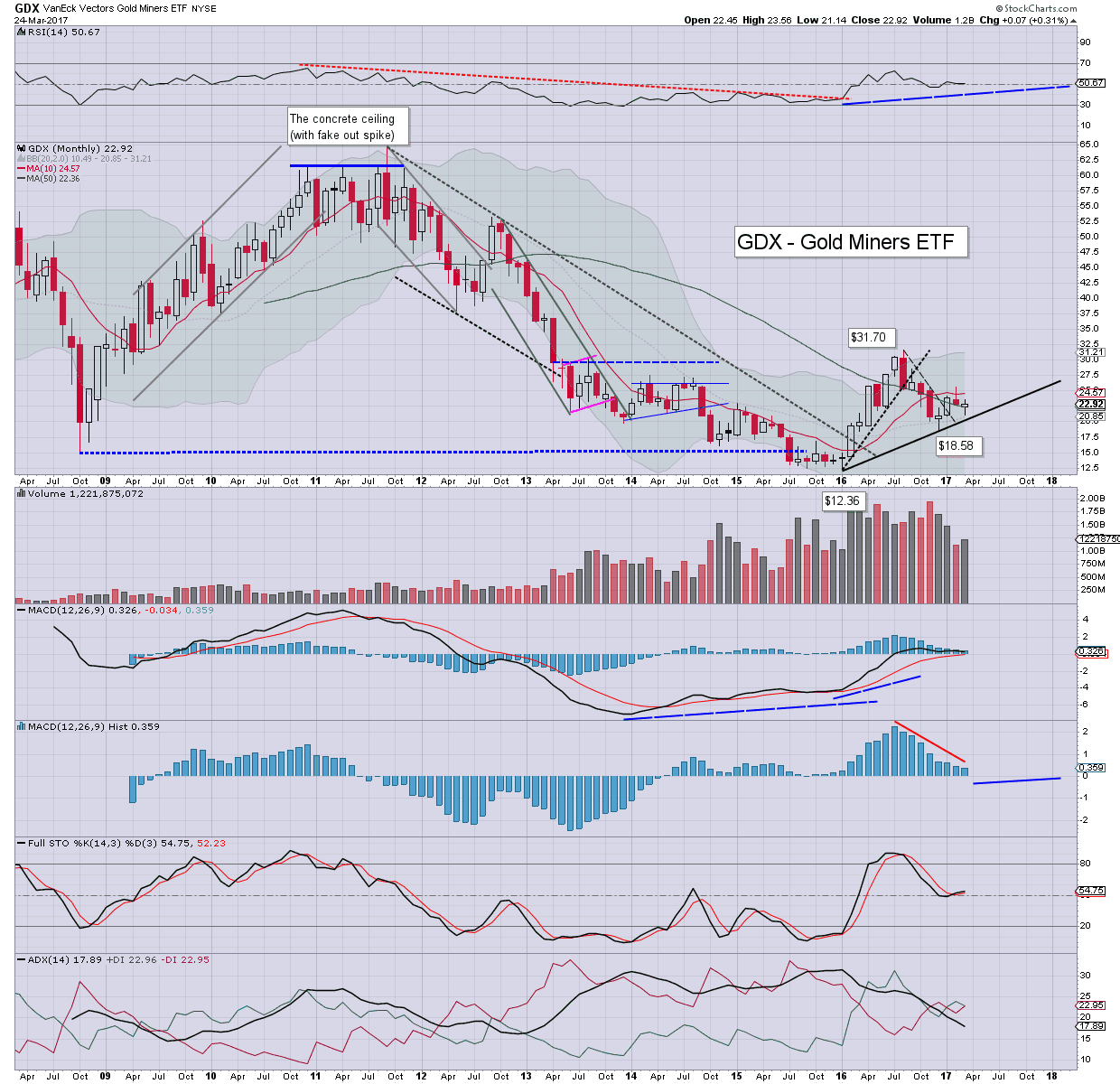

With the precious metals battling upward, the related miners followed. The ETF of GDX settled Friday -0.5% at $22.92, but that still made for a second consecutive net weekly gain of 1.1%. Mid term trend remains bullish, with first big target of the summer 2016 high of $31.70.

GDX, weekly

GDX, monthly

Summary

So... we have another positive week for the precious metals... and related mining stocks.

The key aspect is that the mid term rising trend - that links the Jan'2016 and Dec'2016 lows, remains comfortably intact. In early April, the 'miner bears' would need to see GDX under $21.00 to have provisional confidence that the summer 2016 high was just another lower high.

Considering 'everything else', I'm still leaning on further mid/long term upside.

Things really only get 'hyper bullish' with GDX in the $32s. If that is seen, then a grander target of $50 will be on the menu within a subsequent 9-15 months.

It was another rough day for Ford Motors (F), which imploded in early trading, after a 'weak guidance' statement was issued, with Ford settling -0.8% at $11.68, the lowest level since early Nov'2016. Outlook is shaky.. even if the main market can rally into April earnings.

--

*This arguably sums up the price action since last Friday...

--

Seriously though, after two months of price chop since early January, we have a breakout... but its to the downside, back to levels from early Nov'2016.

Seen on the multi-year chart, we've yet another failure to break above declining trend/resistance that stretches back to summer 2014. The fact Ford is now in the $11s again, means any hopes of a bullish breakout (>$13) are off the menu until at least the latter half of April.

Ford is one of those companies (along with CAT.. and others), that I want to see break to the upside, to have confidence that the US market will continue to broadly climb across this year.

Today's corp' statement and resultant price action sure has dented my confidence.... much like the trees did to that cliff diving Explorer.

Whilst the main market managed a moderate bounce, there was severe weakness in Sears Holdings (SHLD), which imploded by -12.3% to settled at $7.98. The stock is at historic lows, as the mainstream recognise the company is set to disappear.

SHLD, monthly, (linear scale)

SHLD, daily

Summary

The ongoing story of Sears is more of an academic curiosity than anything related to trading opportunities.

Most have begun to accept that the glory days of retail - via shopping malls, are now long past. The 1980s was arguably the peak, with a lesser burst of interest in the 1990s. With the turn of the 21st century, and the rollout of broadband, online shopping finally became a reality.

Sears - like almost all other retailers, has adjusted to some extent, but its still not been enough.

Whether Sears can even survive as a 'going concern' really doesn't matter. What does matter is that other retailers (M, JCP, JWN) keep pushing to adjust to a more online method of selling... or they won't likely survive either.

Whilst the main market saw significant weakness, there was rather powerful downside in Ford Motors (F), which settled -4.3% to $11.75. The loss of the 200dma is important, and does bode for further weakness to the lower end of the price cluster zone to around $11.60.

F, daily

F, monthly

Summary

Today's third consecutive significant net daily decline is the most bearish price action since July/Aug'2016. Ford is still unable to break the declining trend/resistance that stretches back to summer 2014.

Today's big drop was unquestionably partly due to sig' weakness in the main market. However, the loss of the 200dma is a major problem... with Ford seemingly now set for the mid $11s before a chance at stabilising.

Rising rates a problem?

Something to consider... Ford is seen (by myself included) as an attractive stock because of its yield... roughly 5%.

US Int' rates are in the process of rising from effectively zero to a probable 2% in spring 2018. By definition, that makes Ford's yield 2% less 'relative' to other things. That 2% drop on 5% to 3% is a reduction of FORTY percent. The argument could be made that 'all else being the same'... Ford should be in the $8s.. or even 7s in the first half of next year.

Multi-year downward trend

Price action since summer 2014 has been broadly bearish, with Ford repeatedly unable to clear declining trend. Right now, that is around the $13.00 threshold.

For the 'conservative bullish chasers', there is clearly no hurry to get involved until we see some price action in the $13.00s. For the record, I'm still leaning on an eventual bullish breakout, but its taking much longer than expected.

Whilst the main equity market saw a day of moderate chop, there was very powerful strength in Advanced Micro Devices (AMD), which settled +7.0% at $14.43. Broader price action remains very bullish, and the 25/30 zone appears a very realistic target by year end.

AMD, daily

AMD, monthly

Summary

Mainstream chatter about the next product line of Ryzen chips is really starting to capture attention.

I am something of a tech head (my desktop PC is a self-build), and I regular browse a fair few tech sites. Many of them are now rife with attention on AMD and its Ryzen product line.

The downward trend from mid February came to an end this week. The Gold miner ETF of GDX settled Friday -0.4% at $22.67, but that still made for a significant net weekly gain of 4.2%. With the fed out of the way, the mid term bullish trend is likely in the early phase of resuming.

GDX, daily

GDX, weekly

Summary

As noted last weekend, it had seem that the precious metals - and related mining stocks, were merely being pinned lower, until the fed was out of the way. Indeed, once the FOMC announcement was made, there was a powerful jump in the metals, with the miners exploding higher.

So, we've had four weeks of cooling, and now a sig' net weekly gain, what now?

In theory, the metals/miners, should be able to battle upward. That sure doesn't mean every week has to result in a net weekly gain, but those who are bullish, should be seeking some sig' gains across the next 2-4 months.

A challenge of the summer 2016 highs won't be easy, but is a valid target, even if the USD remains broadly strong around the DXY 100 threshold.

--

For those of you with a serious interest in the Gold Miners, I'm still offering issue'1 of my Gold Miners report.

Whilst the main market saw a day of moderate weakness, there was notable strength in Tesla (TSLA), which settled +2.5% at $262.05. Its truly ironic that despite asking for another billion dollars - inherently diluting existing stock, the market just doesn't care.

TSLA, daily

TSLA, monthly (linear scale)

Summary

So... as expected, Tesla is back to asking the capital markets for more money.

You could justifiably argue its to 'avoid bankruptcy', 'stay afloat'.... or merely to have 'ample liquidity'. Whatever you want to call it, Tesla is a loss making manufacturer of motor vehicles.

This is especially ironic since its customer base is unquestionably upper tier, and thus price really shouldn't matter. Why doesn't Musk think he can charge more for his elite type of vehicles, to at least breakeven?

--

From a pure price perspective, we have a short term floor from the $243/42s. There is clear resistance around $265 - as we also saw today.

More broadly - taking into consideration the main market (seeking sp'2600/700s by year end), a move into the $300s looks pretty easy. Indeed, there is already plenty of mainstream chatter of the 400/500s.. given another 2-3 years.

For the record, I've never traded Tesla... and probably never will. I really like the products, think the CEO is inspiring, but the shear valuation of the company is simply.... insane.

--

For some Tesla insanity... pretty much.. NSFW

yours

waiting for the fully self-driving version in the early 2020s.

With precious metals soaring as the fed is 'out of the way', the related Gold Mining stocks had a powerfully bullish day. The ETF of GDX settled +7.7% at $22.98. Near term outlook is bullish, as a net weekly gain is due. The mid term outlook is bullish, as the July 2016 highs are set to be challenged this summer.

GDX, daily

GDX, weekly

Summary

Higher int' rates are inherently bearish for the precious metals, and by default, the related mining stocks. After all, there is a carrying cost to the metals... and as rates climb, the less attractive the metals are.

However, we're still at exceptionally (if not emergency) level rates, with today's new target range of 0.75-1.00%.

I have little concern until int' rates are at least above 2%, and that looks out of range until at least early 2018.

Whilst the main market saw a day of moderate weakness, there was notable strength in Disney (DIS), which settled +0.7% at $112.31. The break into the $112s opens the door to the 114/115s within the near term. Broader upside to the upper 120s/130s seems a given.

DIS, daily

DIS, monthly

Summary

A key reason for today's kick upward above resistance...

Guggenheim have upgraded DIS from neutral to a buy, with a new target of $128. That is a fair way above current levels, but appears well within range before year end.

If you believe DIS will keep on pushing higher, then you should also be inclined to believe the main market will similarly continue to broadly climb across the year.

It was a very subdued start to the week, with Bank of America (BAC), settling u/c at $25.30. The financials have arguably already priced in this Wednesday's (near certain) rate hike of 25bps. First soft support is the 50dma, which will soon be in the low $24s. A year end close in the $30s is on the menu.

BAC, daily

BAC, monthly

Summary

Suffice to add... higher rates are bullish, especially for the financials.

Clearly, the market now believes int' rates will rise across this year, and probably much of 2018.

Of the many financials, I favour BAC, with JPM a somewhat close second.

--

For those with an interest, I'm still offering issue'1 of my Gold Miners report.

The Gold Miners ended the week on a significantly positive note, with a net daily gain of 2.8% to $21.73. However, that still resulted in a fourth consecutive net weekly decline of -2.1%. The mid term bullish trend remains intact, and for now.. it would seem Mr Market has merely managed to wash out the weaker Gold bugs.

GDX, daily

GDX, weekly

Summary

So, despite ending the week on a positive note, the Gold Miners were still net lower for a fourth week. On balance though, when you consider the wave upward from Dec'2016 to early February, the recent cooling was just that... a cooling/retrace.

Note the MACD (blue bar histogram) on the bigger weekly cycle. We're actually due a bearish cross next week, but I envision a stall in downward momentum, with an upward swing beginning in the latter half of the month.

Keep in mind, rising trend for GDX will be still be close to the $20.00 threshold next week, so the miners could take another hit, and still not break the mid term bullish trend.

Things turn very bullish with price action in the $26s, which will open the way to challenge the Aug'2016 high of $31.70.

--

For those with a serious interest in the Gold Mining stocks and the precious metals...

The precious metals continue to lean weak ahead of next week's FOMC. That is keeping the related miners pinned lower. Barrick Gold (ABX) settled -0.8% at $17.68. For now, the mid term bullish trend - from the multi-year low of Sept'2015, remains comfortably intact.

ABX, daily

ABX, monthly

Summary

Today saw the third consecutive daily close under the 50dma. That sure isn't a good sign, but then ABX - along with all of the other miners, had a powerful run from the Dec'2016 low to mid February. A retrace/cooling cycle was due.. and we've likely seen the bulk (if not all) of the move.

Things remain bullish unless rising trend - linking the Dec'2015 and Dec'2016 lows, is broken. Further, there would only be 'full bearish clarity' if the Dec'2016 of $13.78 is taken out, and that looks extremely unlikely.

Best guess: the miners are close/at a short term floor, with the mid term bullish trend set to re-assert itself into the late spring/early summer.

Things turn hyper-bullish if the July 2016 high of $23.38 is taken out.

--

For those with a serious interest in the precious metals and related mining stocks...

With WTIC oil price seeing a very significant net daily decline of around -5% to the low $50s, energy stocks were naturally on the slide. Apache (APA) and Anadarko Petroleum (APC) settled lower by a rather significant -3.6% and -2.7% respectively. Near term outlook is bearish, as the mid term trend has stalled at major resistance.

APA, monthly

APC, monthly

Summary

*rather than get lost in the minor day to day noise, I have instead highlighted the giant monthly charts to give some real perspective.

--

So... WTIC oil had a very rough day as inventory data came in very mixed, and that naturally dragged the related energy stocks lower. Summer driving season is really not that far off, but for now, inventories are close to historic highs, and its increasingly pressuring prices lower.

Outlook?

I am holding to an inflationary scenario, as interest rates look set to climb - which is inherently bullish for equities and (to some extent) commodities.

Clearly, the issue of over-supply remains a problem, and OPEC is still pretty much only able to threaten with words, rather than actual significant supply cuts. Any sustained price action under the $50 threshold would likely see them respond this spring with another threat/announcement, that would (at least temporarily) kick prices back upward.

The wild card?

Any geo-political upset in the middle east.. or (to a lesser extent) across the world, is always going to threaten a spike higher in energy prices. Its somewhat ironic that many of the more unstable countries would especially benefit with higher energy prices.

--

On balance, I'm still looking for WTIC oil to battle upward to at least the $60 threshold this year. If that is the case, both APA, APC, and most other energy stocks should eventually break above their Dec'2016 highs.

The precious metals - and by default... the related miners, appear to be pinned lower, ahead of the March 15th FOMC. The ETF of GDX settled -0.5% at $21.53. Despite ongoing weakness, the mid term rising trend remains comfortably intact around the $20.00 threshold.

GDX, daily

GDX, weekly

Summary

We have short term weakness from the Feb'8th high of $25.71, to today's low of $21.22. Even a foray into the $20s still won't break the mid term rising trend, that links the Dec'2015 and Dec'2016 lows.

Whether the fed raise rates next Wednesday, or not until May 3rd doesn't much matter. What does matter is that whilst it is true that higher rates aren't bullish for the metals/miners, we're still talking about rates that are still around emergency levels.

Clearly, it will be very important to see GDX break last summer's high of $31.70. Once that is achieved, the grander target is around $50.00.

--

For those with an interest in the precious metals and the related Gold Miners...

Whilst the main equity market saw only moderate weakness, there was more significant downside in some of the oil/gas drillers. Transocean (RIG) settled -3.5% at $13.05. The 12.70/13.00 zone is a clear boundary of support/resistance. The 200dma is lurking in the upper $11s from the gap zone of late Nov'2016.

RIG, daily

RIG, monthly

Summary

Suffice to add... it was the second consecutive day of sig' downside for RIG. Price action since last December has been very choppy, but consistently leaning on the weaker side.

Today's close was a marginal spike from support, the next few days will be interesting, especially with another set of oil inventory reports.

It was a bearish week for the precious metals, and that naturally saw the related miners follow. The miner ETF of GDX saw a very significant net weekly decline of -8.1% to $22.18. For now, the broader trend remains bullish, so long as rising trend (around the $20.00 threshold), and most critical, the Dec'2016 low of $18.58 is not breached.

GDX, weekly

GDX, monthly

Summary

Nothing can go up in a straight line... and we're seeing the metals and miners see the first significant weakness since the key higher low from Dec'2016.

Sure, its been a rough week for the mining stocks, but one down week does not negate the bigger trend. Jan'2016 saw a key multi-year floor for the miners, with a subsequent break of the five year declining trend in Feb'2016.

Most important of all... is the key higher low of Dec'2016. So long as that holds, there is little to be concerned about. I remain of the view that an inflationary outcome is likely.

--

For those of you with a serious interest in the mining stocks, I've a special Gold Miner report

Whilst the main market was weak across the day, there was more significant weakness in Caterpillar (CAT), which settled lower by a very significant -4.2% at $94.39. Broadly though... a major bullish breakout above the $100 threshold remains due... certainly by early summer.

CAT, daily

CAT, monthly

Summary

Along with the main market, CAT saw some moderate weakness across the morning. Things really spiralled though on a news report that CAT offices were being searched as part of some investigation. In the grander scheme of things, such an event is likely just one of those 'sporadic' news stories that really have no bearing on the broader company.

From a price perspective, CAT did break short term rising trend today. Broadly though, we're still very close to recent multi-year highs.

--

If you are bullish the US/world economy, then CAT would be one stock that you should seek a massive bullish breakout this year, above the giant psy' level of $100. If you are on the sp'2600/700 train (as I am), then a year end close in the $110/120 zone would be the valid target.