It was a powerfully bullish month for the gold/silver miners. The ETF of GDX settled the month on a positive note, +3.3% @ $23.92. For the month, GDX gained a very significant 14.4%. Near/mid term outlook is bullish, as the Dec'2016 low appears to be a key higher low, with Jan'2016 now secure as a multi-year floor.

GDX, monthly

GDX, daily

Summary

Suffice to say.... January 2017 arguably confirms Dec'2016 as a key higher low.

Next stop.. a daily close above the 200dma in the mid $24s.

Any weekly closes >$25 will give HIGH confidence that GDX is headed to new multi-year highs. First big target is around $50. I recognise that is a long way up... but then so was my target of the $30/35 zone last Feb'... which was hit in August... 5 months ahead of schedule.

Whilst the main market was broadly weak, there was notable relative strength in Disney (DIS) across the day, settling +1.5% @ $110.93. Near term outlook offers further upside to at least the $115s. The Aug'2015 high of $119.51 is a valid target in February.. as earnings are still due.

DIS, daily

DIS, monthly

Summary

Suffice to add.. DIS really was one of the standout stocks today.

Seen on the giant monthly cycle, underlying MACD (green bar histogram) is set to turn positive at the Wed' Feb'1st open. By definition... the upper bollinger in the $115s remains a very realistic near term target.

More broadly, new historic highs look due. For those seeking sp'2500s this summer/year... DIS is going to need to be in the $130s.

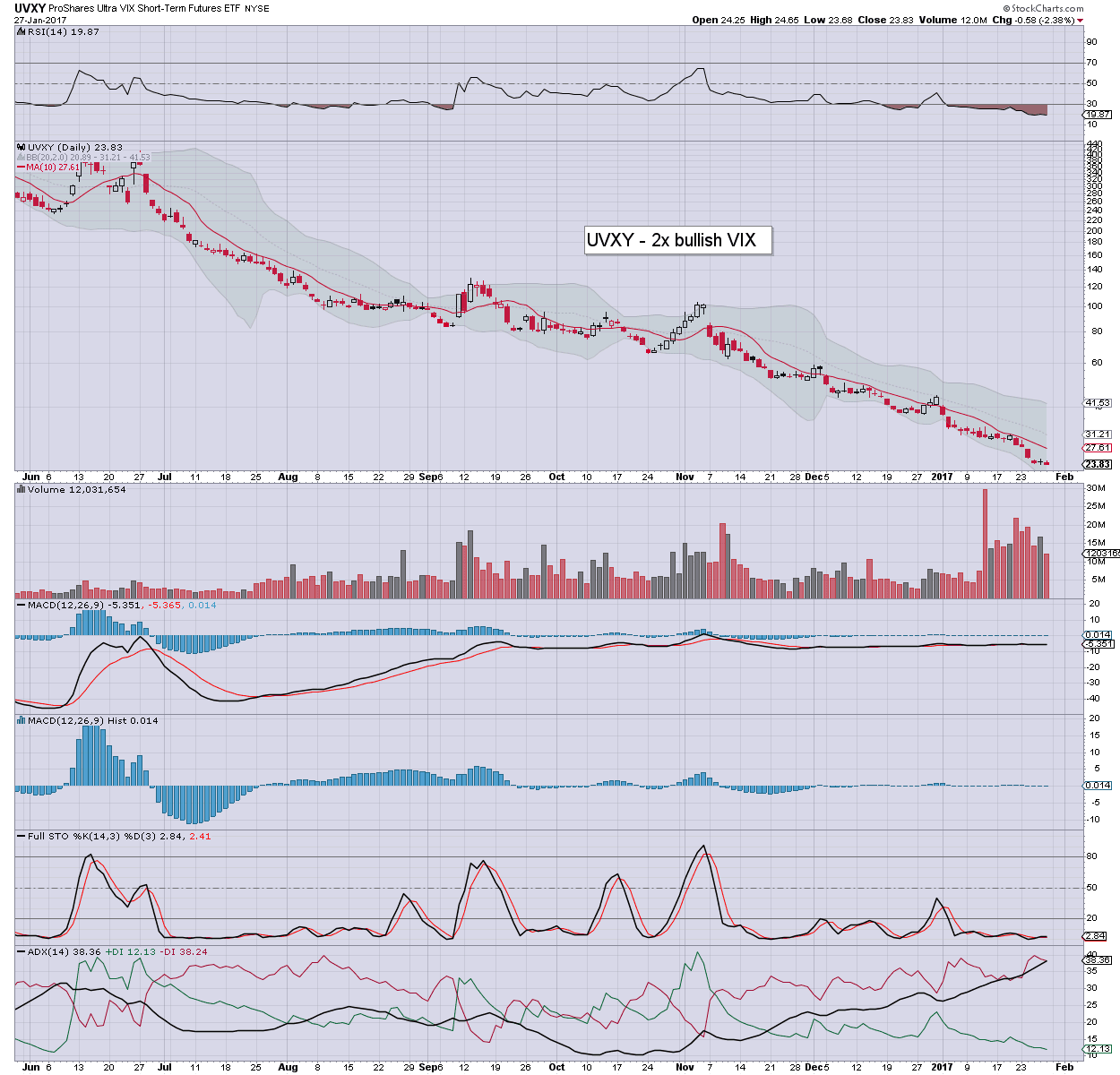

With US equities breaking new historic highs, market volatility remained subdued. The 2x lev' bullish VIX instruments of TVIX and UVXY both saw net weekly declines of -16.1%. Near term outlook offers nothing to the equity bears/volatility bulls.

TVIX, daily

UVXY, daily

Summary

First, an update on the VIX, which saw a net weekly decline of -8.3% .

--

As for TVIX and UVXY, it was a fourth consecutive net weekly decline. Indeed, this was the 10th week lower of the last 12.

--

UVXY recently saw a reverse split... and TVIX will no doubt follow at some point 'soon'.

As ever, holding such leveraged instruments overnight, across the weekend, or worse... across multiple weeks, rarely ends well, not least due to the problem of 'statistical decay'.

--

*yours truly has ZERO interest in being long-VIX for some months to come. Even if the equity market does see a correction of 4-5% in Feb/March... it will do little to kick the VIX higher. The key 20 threshold looks a tough challenge.

Whilst the main market saw a day of moderate chop, there was significant weakness in Ford Motor Co' (F), which settled -3.3% @ $12.37. Price action remains pretty volatile, as Mr Market is waiting for a breakout of the downward trend that stretches back to summer 2014.

F, daily

F, monthly

Summary

re: earnings. As already announced a few weeks ago - when the stock went ex-div', Ford earnings were never going to be great for Q4/2016.

Today, it was a case of 'reasonable earnings... but not great'. That was not enough to inspire any buyers, and the stock rapidly imploded in early morning. Short term rising trend was held though, and things only turn provisionally bearish with price action <$12.20... where the 50 and 200 day MAs are lurking.

--

The bigger picture

Seen on the giant monthly cycle, Ford has been in a broad downward trend since summer 2014.. cooling from the $16s to the 11s. Current declining trend/resistance is around $13.00.

Any price action >13.10 will be decisive enough to break the 2.5yr downward trend, and offer an initial run to the 13.40/80 zone. A test of multi-year resistance of the $16 threshold seems probable this year.

Things turn hyper-bullish with a monthly close >$16. For now.. that is a long way up, but considering the broader market.. does seem a valid target.

Whilst the broader equity market climbed for a second day, there was notable weakness in Freeport McMoran, which imploded at the open on earnings, settling -3.1% @ $16.50. Near term outlook is bearish, but mid/long term, FCX looks headed far higher, not least if Copper can break and hold above the $3.00 threshold.

So, an earnings miss... although far better than a year ago. The real issue that has spooked Mr Market is the Indonesian govt's failure to authorise FCX to export its copper concentrates. Until that is resolved, it will clearly be a drag on the stock price.

However, what should be clear... Mr Inflation is lurking across the world, and Copper prices - having broken upward last November, is headed for the $3 threshold.

Things would become exceptionally bullish for the copper miners, if Copper can attain a monthly close >$3.. which I believe will be the case later this year.

Whilst the main market saw broad strength, there was notable wild price action in the US steel stocks. AK Steel (AKS) saw an early high of $10.26, but then imploded to $8.55, settling -6.6% @ $8.68. Meanwhile, US Steel (X), swung from $34.94, settling +1.3% @ $33.22.

AKS, 15min cycle

X, daily

Summary

First, its notable that this morning, President Trump was signing more things...

A US President that wants infrastructure built... produced by US companies. What a novel thing indeed!

--

As for AKS and X.

I will merely note that both are broadly climbing from their Jan/Feb'2016 lows. Day to day price action remains very volatile.. and today was particularly so with AKS earnings.

There is a great deal of bullish infrastructure talk out there, and it was indeed an inspiring thing to hear the President speak about how we wants pipelines built using US steel. Of course, such capital spending usually takes a very long time (months.... sometimes years) to be agreed at the upper govt' level', and then eventually feeding through to actual companies completing the project.

In any case... for now, the market has rather high hopes that the new President, and his administration will be able to at least see some major projects funded this year. --

Whilst the main market saw some moderate weakness, there was severe downside in Qualcomm (QCOM), which imploded at the open, settling -12.7% @ $54.88. Apple's announcement on Friday that it intends to claim $1bn against QCOM has massively upset the market... with earnings just a few days away.

QCOM, daily

QCOM, monthly

Summary

Pre-market saw the loss of the 200dma, and that really saw the selling intensify. Short term... price action is likely to be volatile... but remaining inclined to the downside. Next support is the big $50 threshold.

I would imagine QCOM and AAPL will eventually be able to agree on something outside of a court, but for now... that could be many... many months away. In the meantime, QCOM now has a $1bn shadow hanging over it.

Keep in mind, QCOM net profit for the year to Sept'2016 was $5.7bn. So... $1bn is still only 20% of one year's earnings. The real problem would be if AAPL decided to go buy its hardware elsewhere.

--

*next QCOM earnings: Wed' Jan'25th.. AH. Market is expecting EPS of $1.18.

With the precious metals somewhat stuck at resistance, the related mining stocks are similarly stuck. The ETF of GDX settled the week net higher by 1.7% @ $23.12. Near term outlook is very mixed, not least as any renewed USD strength will pressure the metals lower, and by default... the related miners.

GDX, weekly

GDX, monthly

Summary

Suffice to add... we are in a mid term upward trend from the Dec'2016 low of $18.58. That remains significantly higher than the Jan'2016 low of $12.36. Broader price structure since last summer is arguably a large bull flag.. or wave'2 retrace.

The 200dma is in the mid $24s. Frankly, I want to see at least the $25s to have some kind of provisional bullish confidence that the $18s were indeed a key higher low.

The super conservative 'bullish chasers' can start chasing with a weekly/monthly close >$27.

Whilst the main market saw moderate price chop, there was significant weakness in US Steel (X), which settled -4.9% @ $33.21. The swing lower was due to renewed chatter about possible oversupply in the steel market. Broadly though.. price action is bullish, and structure is still a big bull flag.

X, daily

X, monthly

Summary

Suffice to add.. price action in X remains very volatile.

Broadly though.. price structure is one big bull flag.. that will be provisionally confirmed with a break into the $36s next week. Things turn extremely bullish with a monthly close >$40.

Whilst the main market was in minor chop mode, those was very significant upside in US Steel (X),which settled higher by a rather powerful 8.3% @ $34.93. Price structure since early December is a very clear bull flag, that will be provisionally confirmed with any price action in the $37s.

X, daily

X, monthly

Summary

Suffice to add... that IS a big bull flag, right? Having ramped from the $17s in early Nov' to the $39s, X has seen around 6 weeks of choppy weakness.

We have a floor around the 50dma of $31.80.

A monthly close >$40 will offer a straight run to $60 within 9-15mths. That might seem overly bullish, but then... I'd merely suggest anyone reflect on the past few months of broad strength.

Whilst the main market began the week on a moderately weak note, there was more significant weakness in financials. Bank of America (BAC) settled -4.2% @ $22.05. Broadly, the 25/26s look a given.. .whether by late spring.. or the summer.

BAC, daily

BAC, monthly

Summary

Friday's daily candle was of the black-fail type, and its not exactly surprising to see that early warning of trouble pan out with significant Tuesday declines.

Broadly though, BAC remains unquestionably hyper-strong. The breakout last Nov' above multi-year resistance of $18, was extremely important. Arguably, its one of the most bullish signals in the entire US equity market.

Mid term target remain the 25/26s... which really aren't that much further to the upside. Its somewhat amusing that no one (that I'm aware of) is yet talking about the $30s.

With the US equity market still regularly breaking new historic highs, market volatility remains very subdued. The 2x lev' bullish VIX instruments of TVIX and UVXY saw net weekly declines of -5.8% and -5.9% respectively. Near term outlook offers little realistic hope that VIX will even break into the mid teens.

TVIX, daily

UVXY, daily

Summary

First, an update on the VIX, which saw a net weekly decline of -0.8%

-

As for TVIX and UVXY... there is nothing to be said other than 'normal service' continues.

--

*UVXY saw a rev' split of 1 for 5 - as of the Jan'12th open. No doubt...TVIX will follow, although nothing is scheduled right now (that I'm aware of).

As ever... holding such leveraged instruments overnight, across the weekend, or worse... across multiple weeks rarely ends well, due to a number of issues, not least 'statistical decay'.

-

Yours truly sees the VIX-long trade as dead, and has ZERO interest in being long the VIX for some months ahead.

Yes, there will be sporadic spikes to the mid/upper teens, and perhaps even test the key 20 threshold this spring. Yet broadly, the US equity market is unquestionably super strong, and that will see the VIX pinned low.

With the US market seeing rather significant falls in early morning, Disney (DIS) was always going to be under pressure, Yet the downgrade from Wieser of Pivotal Research, really was the nail in the coffin, with DIS hitting $107.43, and settling -1.7% @ $107.53.

DIS, daily

Wieser, CNBC call

Summary

Nothing has changed since yesterday....

... other than a rogue research/analyst who has decided to downgrade DIS from $102 to 85. Frankly.. such a downside target is beyond ludicrous.

DIS earnings last November were unquestionably superb. There is absolutely ZERO reason why next earnings - due in early Feb' will be anything other than 'superb'.

The bigger monthly chart continues to be highly suggestive of at least $115 by early Feb'... with an eventual move to new historic highs (>119.51) certainly no later than the early summer.

Whilst the main market closed moderately higher, there was slightly more strength in Disney (DIS) which settled +1.0% @ $109.45. Near term outlook offers the 110/111s before the 3 day holiday weekend. By earnings in early Feb... the $115s look due.

DIS, daily

DIS, monthly

Summary

Suffice to add... short/mid term very strong.

The upper bollinger on the giant monthly cycle is offering the $115s into early Feb'.. when earnings are due. We're due a MACD (green bar histogram) bullish cross in early February... which offers another 3-4 months of basic upside.

Whilst the main market settled moderately higher, there was rather significant upside in Ford (F), which settled +1.7% @ $12.85. An afternoon report that GM will see better than expected capital returns certainly saw 'sympathy' upside in Ford. Mid term outlook to $16, and an eventual hyper push to 23/25.

F, daily

F, monthly

CNBC, screenie

Summary

Recent price action in Ford has been pretty fascinating (and somewhat stomach churning) to watch.

The year end close in the low $12s was ugly, but then two days of upside took Ford to the low $13s. Then the sellers appeared again... whacking Ford to the mid $12s.

Today's report on GM was a classic indirect excuse for renewed upside in Ford.

Any price action >$13.50 will be extremely bullish, and bode for a broader run to test multi-year resistance of $16. I'm of the view we'll break through it... much as BAC broke >$18 in November.

Whilst the broader market began the week on a moderately weak note, there was notable strength in tech, with Apple (AAPL) settling +0.9% @ $118.98. The near/mid term outlook is bullish to the $120/125 zone. The April 2015 historic high of $131.29 looks set to be broken at some point.

AAPL, daily

AAPL, monthly

Summary

Without getting lost in the minor short term noise, I'd suggest anyone note price structure on the giant monthly cycle. Upper bollinger is offering the $125s in the near term, although that would still be some 5% below the 2015 high - back when the sp'500 was maxing out in the low 2100s.

--

Pete Najarian on CNBC highlighted a MS target for AAPL of $148.

That seems viable by late 2017, but assumes no sig' market retraces >10%.

With US equities starting the year on a pretty bullish note, volatility was ground broadly lower. The 2x lev' bullish VIX instruments of TVIX and UVXY both saw a rather severe net weekly decline of -25.6%. Near term outlook offers little to the volatility bulls, as equities remain broadly strong.

TVIX, daily

UVXY, daily

Summary

First, an update on the VIX, which saw a net weekly decline of -19.4%.

--

As for TVIX and UVXY, there is little to add. Today's settlements were at new historic lows, but then, such instruments decay across the mid term anyway.

To me, the VIX-long trade remains dead. There are clearly going to be sporadic jumps in the VIX in 2017, but for now... even a brief move to the key 20 threshold looks out of range.

--

*TVIX/UVXY will likely be due another reverse split within 3-4 months.

With the USD significantly lower, the precious metals were kicked an extra bit higher today. The related mining stocks were naturally also on the rise, with the ETF of GDX settling +5.8% @ $23.19. There is a clear bullish breakout now underway.

GDX, daily

GDX, monthly

Summary

Suffice to add... we have a provisional bullish breakout. The only thing left to clear is the 200dma in the mid $24s.

Any price action in the $25s will turn the broader mid term trend bullish, and be HIGHLY suggestive that the recent low of the $18s was a key higher low.

If that is the case.. first big target is $50.... and that is a very long way higher indeed.

Whilst the main market saw a second day of broad gains, there was very significant upside in Ford (F), which settled higher by a powerful 4.6% @ $13.67. Near term outlook is bullish, with a basic mid term target of $16 by the summer. Any monthly close >16 offers hyper upside to 23/25.

F, daily

F, monthly

Summary

Last Friday saw the main market help drag Ford down to a low of $12.08... having cooled from $13.20.

Its taken Ford just two trading days to break back into the low $13s.

There are multiple aspects of resistance in the low $13s.. not least as seen on the giant monthly cycle.

Any price action >13.50 will be decisive enough to clarify further upside to the $14 threshold. Any daily closes in the $14s will offer a fast run to multi-year resistance of the $16 threshold.