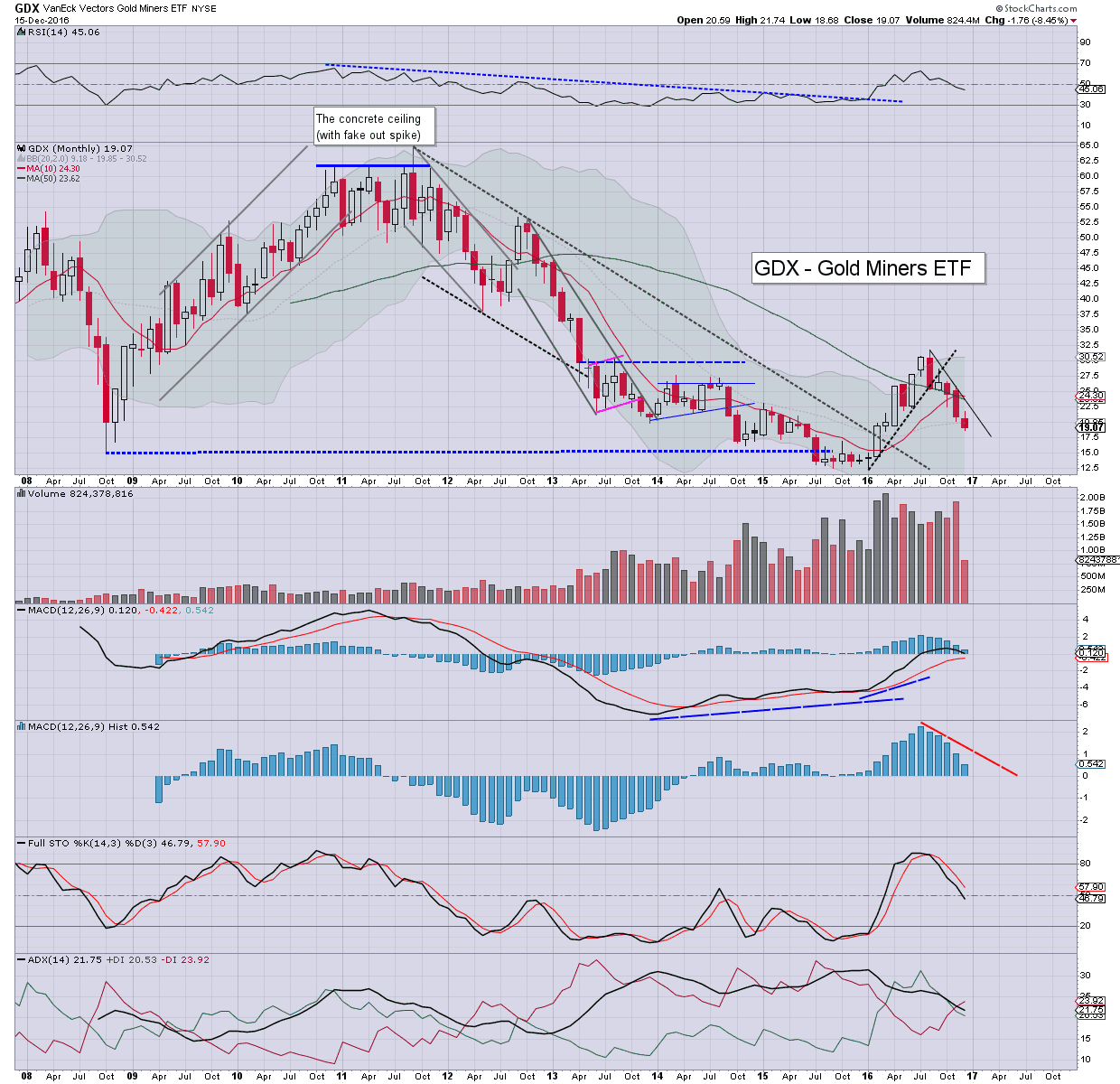

GDX, daily

GDX, monthly

Summary

First, I'd suggest you also go check my year end update for Gold and Silver... which should appear by late Friday night.

--

In early trading GDX seemed set for a year end close above the 50dma...but failed. Its not a great sign, and with gold/silver still within mid term downward trends, the short/mid term outlook for the miners remains bearish.

That only provisionally changes with GDX in the $23s.

For full bullish clarity, I want to see a monthly close in the $25s.

--

Its notable that GDX saw a Jan'2016 low of $12.36, hyper-ramping to a peak in Aug' at $31.70, and then cooling by around a third, to settle the year net higher by 52.5%. On any basis... a bullish year, but as noted, there is clearly still a threat of further downside, as Gold and Silver both remain mid term bearish.